Since November 29, 2011 Standard & Poor’s Ratings Services has applied its revised rating criteria to 126 bank groups in the Asia-Pacific region and published the ratings via group media releases and individual reports. Including the subsidiaries, a total of 208 entities were covered.

How do Asia-Pacific bank ratings and ratings distributions fare compared with their global peers after application of the revised criteria?

The impact of the application of new criteria on the issuer ratings on Asia-Pacific banks is smaller than that globally. Among the 126 ratings on financial institutions in the Asia-Pacific region (which does not include subsidiaries of banking groups and holding companies), 68% of ratings were unchanged, while 57% were unchanged globally.

The distribution of rating changes in Asia-Pacific is broadly similar to that globally. The application of new criteria resulted in higher ratings for 20%, lower ratings for 12%, and the same ratings for 68% of the total groups.

What is the key factor that resulted in the downgrade of banks in Australia and New Zealand?

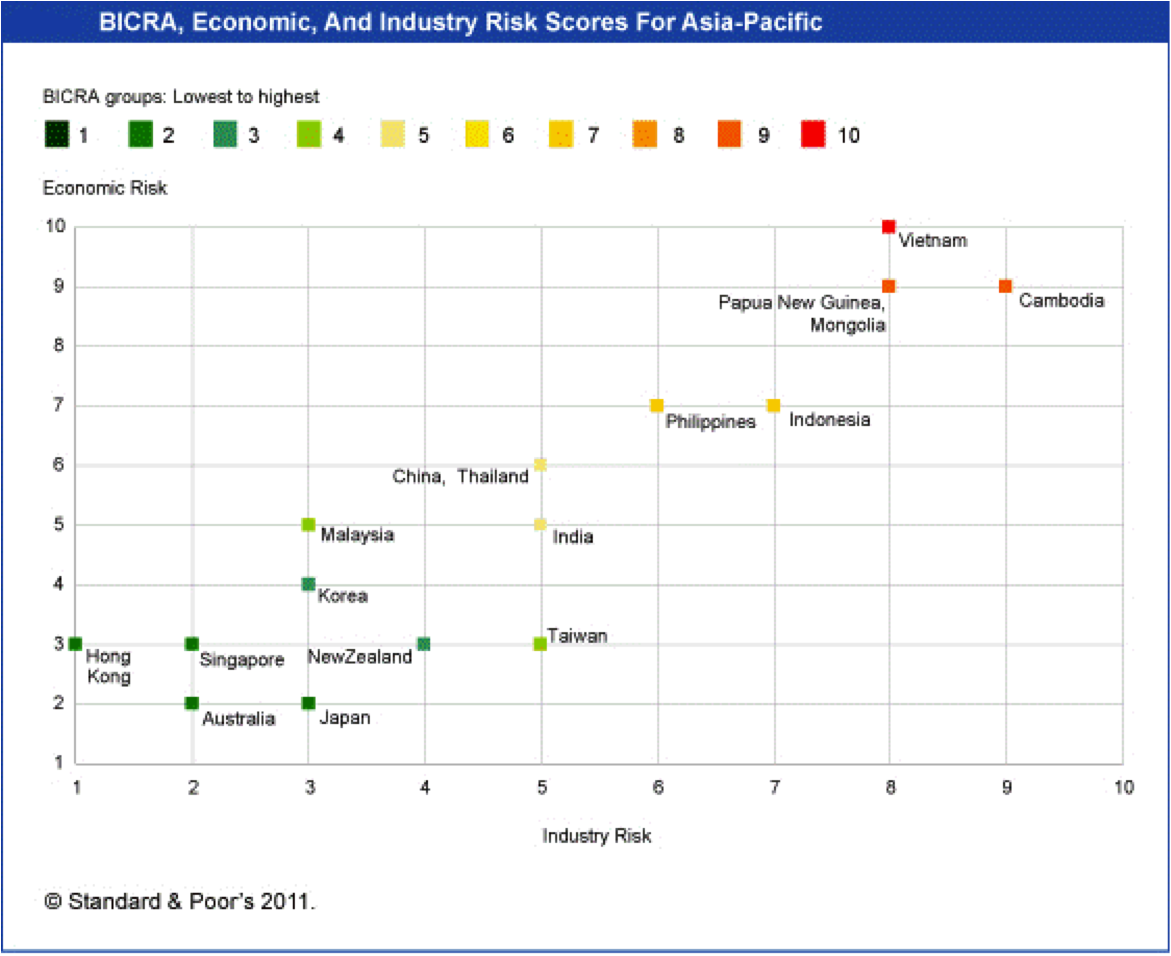

We lowered a number of ratings on banks in Australia and New Zealand following our review under the revised criteria. Similar to ratings on banks in other countries, and in line with our updated criteria, ratings on Australian and New Zealand banks are materially influenced by Banking Industry and Country Risk Assessment (BICRA) scores in these banking systems, as they contribute to the anchor for any bank rating (see chart 1).

These downgrades do not generally indicate that we consider the risk in these banking systems to have incrementally increased in the past year, or that the banks' operating performance has weakened during this time. Rather, these downgrades are driven largely by a recalibration of our criteria. A critical new feature of the revised criteria is the explicit and substantial impact of BICRA scores on a bank rating.

Does improvement in a BICRA score always lead to a higher rating?

Under the new criteria, the BICRA scores on China, India, Korea, Indonesia, Thailand, The Philippines, and Cambodia have improved. Although there are some higher ratings in China, Korea, and The Philippines, the improvement in BICRA scores have not resulted in an automatic upgrade of all banks in such systems. This is because under our previous methodology, BICRA scores did not have an explicit or substantial impact on bank ratings. In addition, bank ratings incorporate bank-specific factors and external support factors, in addition to the anchor assessment. In the future, a change in BICRA score could indeed be expected to put pressure, in a similar direction, on bank ratings in that system because the anchor assessment is generally driven substantially by the BICRA scores on the domestic banking system (see chart 2).

As the world’s growth engine in recent years, is China playing an increasingly influential role in the region’s banking sector?

Given China’s sizeable economy and connections within Asia-Pacific and the world, its performance is one of the key credit sensitivities for many banks in the region and could generate ripple effects globally. While we assigned a BICRA score of '5' to China, which is slightly higher than the average score for Asia-Pacific, we recognize the “high risk” of economic imbalance in China, as well as its high credit risk. Significant adverse economic developments in China are likely to generate much bigger shocks than most other Asia-Pacific economies. Such a negative impact would be felt by economies that supply raw materials or semi-finished goods to Chinese industries.

Which countries in the region benefit from a rating uplift due to strong government support?

The positive rating actions in China, Japan, Singapore, Korea, and Hong Kong factor in the recognition in our criteria of the potential for future extraordinary government support in a more explicit manner. Of the 25 bank groups upgraded, the issuer credit ratings of only four do not incorporate the likelihood of extraordinary government support. Of all the rated 126 bank groups in Asia-Pacific, the issuer credit ratings of more than half include an uplift due to the likelihood of extraordinary government support. In addition, 17% of the bank groups are classified as government-related entities (GREs) or "systemically important" banks, and their issuer credit ratings do not incorporate any support as their stand-alone credit profiles (SACPs) are the same as the foreign-currency ratings on the sovereign (see chart 1).

For instance, Standard & Poor's has incorporated uplifts from likely government support into the ratings on four major Chinese banks. We view these banks as GREs, given their strong government links and their roles in supporting government economic policies. Under our methodology, the vast majority of governments in the Asia-Pacific region are assessed as "highly supportive." This means we believe almost all governments in the region would likely take proactive measures to ensure full and timely payments to senior creditors of the banking sector.

Is funding and liquidity an area of strength for banks in the region?

We see funding and liquidity as an area of relative strength for Asian banks. Our assessment of funding and liquidity is a positive factor for the SACPs on banks in six countries: China, India, Japan, Malaysia, Taiwan, and Singapore. While the systemic advantage of abundant domestic deposit funding is captured in our BICRA analysis, the relative advantage of large banks in these systems is captured in their funding and liquidity assessment. These banks tend to have large portions of their liabilities made up of stable core deposits, and a low reliance on wholesale funding. The loan-to-deposit ratios of most Asia-Pacific banks are generally low by global comparison.

The banking systems in Australia, New Zealand, and Korea have a higher dependence on wholesale funding—a factor that affects the anchor of all bank ratings in these systems through our industry risk score within the BICRA assessment. In addition, ratings on a large number of banks in Australia and New Zealand are further negatively adjusted due to our assessment of their funding profiles as “below average.” Nevertheless, we do not consider this adjustment to be a “double count” of the systemwide funding weaknesses. We have applied this adjustment to banks whose funding profiles we consider to be weaker than the average for the banking system. The Australian and New Zealand banking systems are dominated by four major banks in each country. Therefore, we consider that under a stress scenario, most of the smaller institutions--which are relatively large in number, are likely to face greater challenges in retaining their deposits than the four major banks, notwithstanding often better funding ratios seen for the smaller institutions. The funding profiles for the major banks in these two systems have been scored "average."

Three Korean policy banks are scored "below average" funding, mainly due to their dependence on wholesale funding, which we believe is greater than the average of the Korean banking industry.

What is Standard & Poor’s outlook for Asia-Pacific banks in general?

The outlooks for 79% of bank groups in Asia-Pacific are stable, reflecting the sound financial profiles of the banks and the region's relatively strong economic prospects. They also reflect the currently stable outlooks on the majority of the sovereign ratings in Asia-Pacific; with bank and sovereign ratings having become more directly linked under the new criteria.

Two notable exceptions are the sovereign ratings on Japan and Vietnam, which have negative outlooks. Seventeen Japanese banks and two Vietnamese banks have negative outlooks as most of these banks benefit from potential future government support and the negative rating actions on sovereign ratings could result in lower ratings on many of these banks. In addition, any deterioration in sovereign creditworthiness could have various direct and indirect impact on bank ratings as it leads to changes in BICRA scores, worsening asset quality, and higher funding costs.

Are Asia-Pacific banks immune from global economic downturn and the debt crisis in Europe?

Although we do not foresee material changes in the creditworthiness of the banking industry in the Asia-Pacific region, we also do not see it as likely to decouple from the downside risks facing the global economy, in particular the ongoing sovereign debt crisis in Europe and the sluggish US economy. The eurozone crisis has already caused actual economic growth in 2011 in many Asia-Pacific countries to be slower than we earlier projected, and the outlook for 2012 will depend largely on the resolution of eurozone concerns and US economic growth. With the region's strong economic prospects--which have been the biggest supporting factor for the credit profile of Asia-Pacific banking systems--coming under pressure, we see moderation in nonperforming loans and credit provisioning as likely to reverse. This could lead us to lower our assessment of banks' risk positions and capital and earnings. This trend is likely to be more pronounced in banking systems with high inflation, such as India and Vietnam, and recent high credit growth, such as China, Hong Kong, and India. Should the persistence or a worsening of the eurozone crisis lead to a squeeze in funding markets, higher wholesale funding costs, combined with lower loan demand, is likely to put some pressure on Australian and Korean banks' profitability. However, we do expect the central banks of these countries to step in to provide liquidity support, if needed.

Nevertheless, we currently view most banks in Asia-Pacific as relatively well positioned to withstand these pressures within the current ratings levels. In our base-case scenario, we expect the Chinese banking system to withstand losses from real estate and local government-related loans. Even in a worst-case scenario, the sector would receive financial support from the government given its importance to the economy. Given the still-positive economic growth prospects for Asia-Pacific, the region's healthy household and corporate sectors, and the generally sound financial profile of Asia-Pacific's financial institutions, we do not expect many, if any, rating changes to result.