The global “wall” of non-financial corporate debt maturities coming due from 2012 to 2016 is not new to market observers. Less discussed is the incremental financing that corporate debt issuers will need over this period to fund capital expenditure and working capital growth.

What are the challenges facing global corporate credit markets?

The sovereign debt crisis in Europe, regulatory pressure on banks and the potential of a hard landing for the Chinese economy have resulted in a fragile recovery for the world economy. Standard & Poor’s expects the demand for funds in the next five years will potentially compound the credit rationing that may occur as banks seek to restructure their balance sheets, and bond and equity investors reassess their risk-return thresholds.

What is the size of refinancing and new money requirements needed over the next five years?

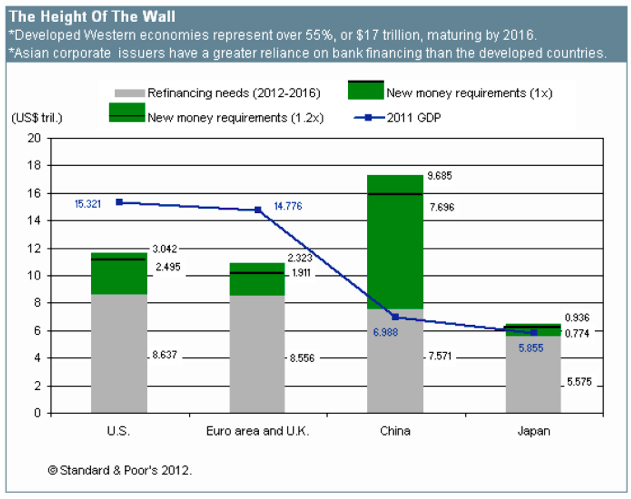

We estimate that the bank loan and debt capital markets will need to finance a $43 trillion to $46 trillion wall of corporate borrowings between 2012 and 2016 in the US, the eurozone, the UK, China, and Japan (including both rated and unrated debt, and excluding securitised loans, see chart 1). This amount comprises outstanding debt of $30 trillion that will require refinancing, plus $13 trillion to $16 trillion in incremental commercial debt financing during the next five years that we estimate companies will need to spur growth (see table 1).

Chart 1

What about the size of refinancing and new money needed for China and Japan?

We expect the refinancing requirement for China to be around $7.6 trillion between 2012 and 2016. This amount should not pose too much of a problem for China’s state-owned banks, which make up about 75% of the country’s overall banking sector. They are likely to roll over loans extended to state-owned enterprises (SOEs), which contribute about 35% of total annual fixed-asset investments in China. In terms of new financing needs, we estimate that China may need between $7.7 trillion to $9.7 trillion (see table 1), which is a very large amount. The amount, more than the combined estimated new financing needs of the eurozone, UK and US, is driven by the high assumed nominal GDP growth of 12% a year for China. In contrast, we estimate only a 2% nominal growth for Japan, which results in estimated new financing of $770 billion to $940 billion.

Table 1

Can you explain your concerns about incremental financing needed versus refinancing?

We believe that banks and capital markets should be able to replace old debt, but credit rationing may limit new bank financing needed to fund growth.

It is our working assumption that global banks and debt capital markets will largely be able to continue to provide the majority of liquidity to allow most corporate issuers to proactively manage their forthcoming refinancing. However, the balance is fragile, and credit rationing may constrain banks from rolling over loans to some leveraged borrowers, limiting the availability of new term bank financing to fund growth.

While we expect that the relatively mature debt markets in the US, with its demonstrated ability during the past three years to provide more than $400 billion a year of new corporate funding, are in a good position to make up any shortfall, the European corporate bond market remains less developed. As such, if we assume European corporate issuers tapped the bond market for 50% of their respective new funding requirements (up from about 15% historically), this would imply $210 billion to $260 billion of net new yearly issuance by European non-financial corporate borrowers. There have only been two years during the past decade when net new issuance by eurozone companies has exceeded $100 billion. While this presents a significant growth opportunity for European debt market investors, it also highlights the challenges confronting non-financial corporate borrowers in Europe, especially if they are forced to turn to a more sought-after US debt market for alternative funding.

What constitutes a “perfect storm”?

In a perfect storm, the European banks are unable to fulfil capital strengthening plans, the eurozone crisis deepens, the Chinese economy suffers a hard landing, the asset quality of banks deteriorates further, oil prices continue to rapidly escalate, commodity prices become even more volatile and inflation re-emerges.

Do government and capital markets have capacity to provide the new “bricks” needed to extend the maturity wall and spark economic growth?

It depends on the continued ability of banking system regulators to lead a path through the minefield that lies ahead. Governments and central banks globally have used many financial tools in their arsenals to stabilise the financial system and strengthen bank balance sheets. In conjunction with the global financial markets showing signs of stability, monetary and fiscal policies quickly shifted to focusing on restoring economic stability and growth. However, this highly accommodative monetary policy, centred on expanding the monetary base and maintaining artificially low interest rates, is likely to produce only a fragile recovery at best, and could easily be thrown off course at any moment. The main risks that could challenge the policy consensus include a backlash to the austerity measures introduced in debtor countries in Europe, escalating oil and commodity prices (possibly triggered by further geopolitical unrest in the Middle East) and a potential material slowdown of growth in China.

Will the increasingly difficult bank operating environment affect lending capacity?

Credit rationing could restrict global loan growth in the future as new term bank financing becomes difficult to secure. While most of the economic and regulatory challenges facing the banks are similar in both the US and Europe, we believe that most of them will have a more severe effect on lending capacity in Europe. Specifically, European banks have to adapt to a weaker economy and uncertainties relating to sovereign debt sustainability, while managing more highly levered balance sheets. The faster implementation of the Basel III timetable only heightens the challenge for European banks. Inevitably, this will have a more profound effect on corporate borrowers in Europe because of their greater dependency on relationship banks to provide funding.

Similarly, US banks may limit loan growth because of their higher regulatory cost of capital, but the potential to voluntarily return excess capital to shareholders may also act as an additional constraint. Asian banks are likely to continue lending, although at a slower rate in line with lower economic growth. In some Asian countries, such as China, a significant portion of bank lending may be indirectly state directed; therefore, lending capacity is not subject to the same limitations as in Western markets.

What are your biggest concerns for China in case of a hard landing scenario?

We forecast a one-in-10 chance of a hard landing scenario in China of 5% growth. In case there is a hard landing in China, our two biggest concerns are the property sector and local government, particularly the local government financing vehicles. These are the two weak spots for the country’s economy. We consider that more highly rated real estate issuers should be able to endure a significant slowdown. However, those rated in the ‘B’ rating category would be most vulnerable, especially in a hard landing, with their inherent liquidity challenges possibly causing some to default.